The Employee Retirement Income Security Act of 1974 (ERISA) is a federal law that sets minimum standards for employee benefit plans maintained by private-sector employers. Under ERISA, employer-sponsored welfare benefit plans, such as group health plans, must be described in a written plan document. In addition, employers must explain the plans’ terms to participants by providing them with a summary plan description (SPD).

The insurance certificate or benefit booklet provided by an insurance carrier or other third party for a welfare benefit plan typically does not satisfy ERISA’s content requirements for plan documents and SPDs. However, employers may use wrap documents in conjunction with the insurance certificate or benefit booklet in order to satisfy ERISA’s requirements. This document is called a “wrap document” because it essentially wraps around the insurance certificate or benefit booklet to fill in the missing ERISA-required provisions. When a wrap document is used, the ERISA plan document or SPD is made up of two documents— the insurance certificate or benefit booklet and the wrap document.

LINKS AND RESOURCES

- Reporting and Disclosure Guide for Employee Benefit Plans

- ERISA Section 402 – plan document requirements

- ERISA Section 102(b) and DOL Reg. §2520.102-3 – SPD requirements

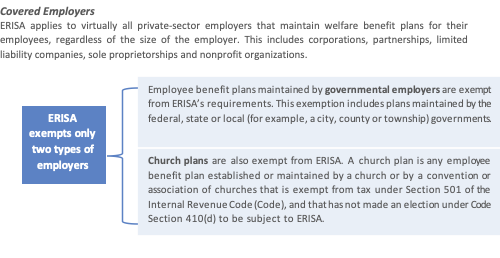

ERISA Coverage

Small employers are subject to ERISA’s requirements, unless they meet the exemption for governmental employers or churches.

Welfare Benefit Plans

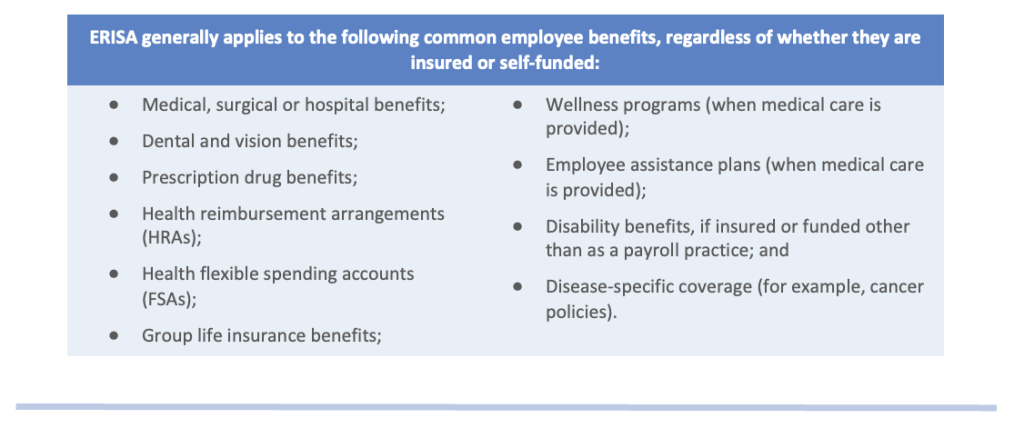

Many employment plans or programs that provide nonretirement benefits to employees are considered employee welfare benefit plans that are subject to ERISA. To qualify as an ERISA plan, there must be a plan, fund or program that is established by the employer for the purpose of providing ERISA-covered benefits (through the purchase of insurance or otherwise) to participants and their beneficiaries.

Written Plan Document

ERISA requires welfare benefit plans to “be established and maintained pursuant to a written instrument.” Thus, an employer’s welfare benefit plans must be described in a written plan document. There is no small employer exception to ERISA’s plan document requirement.

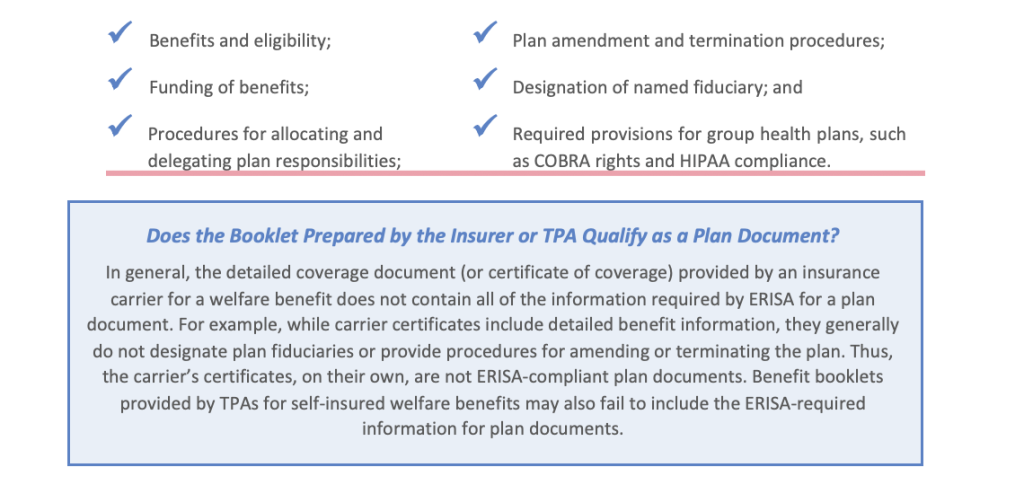

ERISA does not require that a plan document be in any particular format. However, there are several topics that must be addressed in the written plan document for a welfare benefit plan. For example, the plan document must address:

Wrap Documents

A wrap document is a relatively simple document that supplements existing documentation for a welfare benefit plan (for example, an insurance certificate or benefit booklet). This document is called a wrap document because it essentially wraps around the certificate or booklet to fill in the missing ERISA-required provisions. Because the wrap document incorporates the insurance certificate or benefits booklet by reference, the plan’s benefit provisions continue to be governed by the terms of those documents.

When a wrap document is used, the ERISA plan document is comprised of two pieces:

| 1 | The insurance certificate or benefits booklet, reflecting many of the plan’s important terms and requirements; and |

| 2 | The wrap document that fills in the ERISA-required information that is missing from the insurance certificate or benefits booklet. |

Mega Wrap Plans

Wrap documents can be used to combine more than one welfare benefit under a single plan, which is sometimes referred to as a “mega wrap plan” or an “umbrella plan.” For example, a wrap document could be used to bundle medical benefits, dental benefits, disability coverage and an HRA under one single ERISA plan. This document would wrap around all the third-party documentation (for example, insurance certificates or benefit booklets) to include the missing ERISA provisions and combine the benefits into one plan.

The decision of whether to combine (or bundle) welfare benefits often depends on how it will affect the Form 5500 filing obligation.

- For larger employers, combining different benefits together may simplify the annual reporting requirement because only one Form 5500 will be required for the bundled plan.

- For smaller employers, however, each benefit offered as a separate plan may qualify for the Form 5500 exemption for small plans. Combining the benefits together under a bundled plan might cause the plan to exceed the threshold for small plans, which would trigger the Form 5500 filing requirement.

Summary Plan Descriptions

Virtually all welfare benefit plans that are subject to ERISA must provide participants with an SPD, regardless of the size of the sponsoring employer. An SPD is a document that is provided to plan participants to explain their rights and benefits under the plan document. ERISA also includes detailed content requirements for welfare benefit plan SPDs.

In general, a carrier’s insurance certificate will not include all the information that must be included in an SPD under ERISA. A benefit booklet prepared by a TPA may also fail to include the ERISA-required information for SPDs. To create an SPD in this situation, an employer can use a wrap document (wrap SPD) that includes the ERISA-required information that the certificate or booklet prepared by the insurer or TPA does not include. In this scenario, the wrap SPD and the insurance certificate or booklet, together, make up the plan’s SPD. To comply with ERISA, both the wrap SPD and the insurance certificate or booklet must be distributed to plan participants by the appropriate deadline.

Noncompliance

There are no specific penalties under ERISA for failing to have a plan document or SPD. However, not having a plan document or SPD can have serious consequences for an employer, including the following:

- Inability to respond to participant requests: The plan document/SPD must be furnished in response to a participant’s written request. The plan administrator may be charged up to $110 per day if it does not provide the plan document within 30 days after an individual’s request. These penalties may apply even where a plan document/SPD does not exist.

- Benefit lawsuits: Not having a plan document may put an employer at a disadvantage in the event a participant brings a lawsuit for benefits under the plan. Without a plan document, it will be difficult for a plan administrator to prove that the plan’s terms support benefit decisions. Also, without a plan document, plan participants can use past practice or other evidence outside of the actual plan’s terms to support their claims. Additionally, courts will likely apply a standard of review that is less favorable to the employer (and more favorable to participants) when reviewing benefit claims under an unwritten plan.

- DOL audits: The Department of Labor (DOL) has broad authority to investigate or audit an employee benefit plan’s compliance with ERISA. When the DOL selects an employer’s health plan for audit, it will almost always ask to see a copy of the plan document and SPD, in addition to other plan-related documents. If an employer cannot respond to the DOL’s document requests, it may trigger additional document requests, interviews, on-site visits or even DOL enforcement actions. Also, the DOL may impose a penalty of up to $190 per day (up to $1,906 per request) for failing to provide information requested by the DOL.

This Compliance Overview is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice. ©2018-2024 Zywave, Inc. All rights reserved.